Expert verified

Expert verified Tax deductions for self employed professionals can remarkably reduce the amount of tax you owe while also helping you manage your business finances efficiently.

In this blog, we break down all the expenses that qualify as deductions from health insurance to the cost of running a business.

Business Expense Deductions: What Qualifies?

The Income Tax Act allows freelancers, consultants, sole proprietors, or independent professionals, to deduct expenses that are directly related to running a business.

The business expense can be claimed as a deduction while calculating taxable income under the head “Profits and Gains of Business or Profession.”

Let’s break it down:

Section 37(1)

It serves as the primary provision for deducting business expenses. To qualify as a deductible expense, it must meet four conditions:

- Expense must be incurred wholly and exclusively for business or professional purposes

- Must not be a personal expense

- Must not be capital in nature (capital assets are claimed through depreciation instead)

- Must not be specifically disallowed under the Act

This means that if an expense helps you earn or maintain business income and is properly documented, it is deductible.

Example: A freelance graphic designer paying for Adobe Creative Cloud can claim the cost as business expense.

Common Business Expenses Self-Employed Professionals Can Deduct

Most freelancers and small business owners incur recurring operational expenses that qualify for deductions:

Office and Workspace Costs

Expenses related to maintaining a workspace are deductible if they are used for business purposes.

- Office rent or co-working space membership

- Electricity and internet used for business operations

- Office furniture and supplies

- Repairs or maintenance related to office premises

If you operate from home, you may claim a proportionate share of rent, electricity, and internet bills. This is based on the portion of the home used exclusively as a workspace.

So, if one room out of a four-room home is used solely as an office, roughly 25% of eligible household expenses may be claimed as business expenses.

Operational and Technology Costs

Many self-employed professionals use digital tools and platforms. These expenses are fully deductible if used for business.

- Accounting software such as Zoho Books or QuickBooks

- Design or productivity software

- Cloud storage subscriptions

- Website development, domain registration, and hosting fees

- Payment gateway charges and bank transaction fees

These costs are considered ordinary and necessary business expenses, especially for freelancers working in digital or service industries.

Professional Fees and Services

Expenses incurred for professional support services are also deductible.

- CA or tax consultant fees

- Legal services related to contracts or compliance

- Payments to subcontractors or freelancers working with you

- Business insurance premiums such as professional indemnity insurance

- Industry memberships and professional association fees

Example: If a marketing consultant hires a freelance copywriter for a client project, the payment made to that contractor can be claimed as a business expense.

Travel and Client-Related Expenses

Travel costs that are directly linked to business activities can also be deducted.

- Flights, train tickets, or taxi fares for client meetings

- Hotel stays during business travel

- Local conveyance such as fuel or ride-hailing services for work purposes

- Event or conference travel related to professional development

Again, the expense has to be related to business activities and is to be supported by invoices or travel records.

Also Read: How you can save tax when buying a car

Marketing and Business Development Costs

Promoting your business is another legitimate deductible expense.

- Digital advertising on platforms such as Google. Meta or social media

- Branding and logo design

- Printing business cards or brochures

- Email marketing tools or CRM software

Example: A small consulting firm running Google Ads to generate leads can claim the full advertising spend as a business deduction.

Education and Skill Development

Training that improves or maintains skills related to your current profession can be deducted.

- Professional workshops or seminars

- Industry certifications

- Online courses directly related to your field

Example: A photographer attending a professional editing workshop qualifies for this deduction.

Here, courses that prepare you for an entirely new career path, generally do not qualify.

Depreciation on Business Assets

Capital assets such as laptops, cameras, furniture, and vehicles cannot be claimed as a one-time expense.

Instead, their cost is deducted gradually through depreciation under Section 32 of the Income Tax Act.

Common depreciable assets:

- Computers and laptops

- Office furniture

- Cameras or production equipment

- Vehicles used for business purposes

Depreciation rates are prescribed under the Income Tax Rules and allow you to spread the deduction across multiple years.

Expenses That Are Not Deductible

| Expense | Why It’s Disallowed |

| Personal travel mixed with business | Only the business portion is deductible; mixed trips need clear bifurcation |

| Fines and penalties | Expressly disallowed under Section 37(1) |

| Capital expenditure (e.g., buying a laptop outright) | Claimed via depreciation, not as a direct expense |

| Personal food, clothing, or lifestyle costs | No business nexus |

| Cash payments above ₹10,000 to a single party in a day | Disallowed under Section 40A(3) |

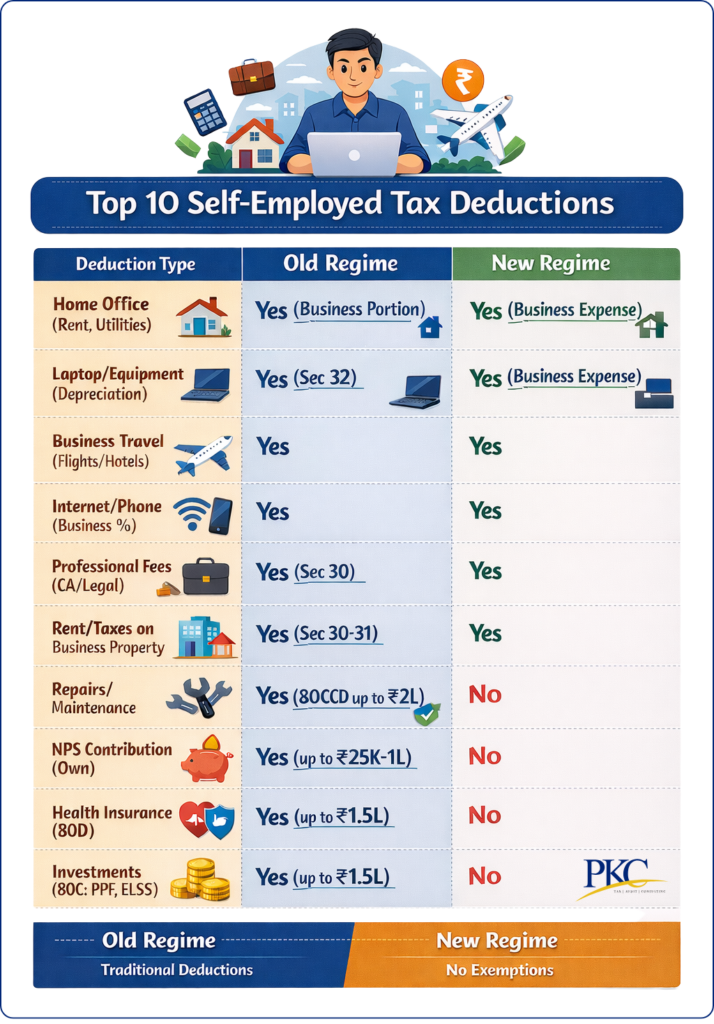

Section 80C, 80D, 80E: Deductions for Self-Employed

Chapter VI-A of the Income Tax Act allows self-employed individuals to claim deductions for investments, insurance, and education loan interest.

However, these deductions apply only if you opt for the old tax regime. In the new tax regime under Section 115BAC, most of these benefits are not available.

Section 80C: Investment-Based Tax Savings

Allows individuals, including self-employed professionals, to claim deductions of up to ₹1,50,000 per financial year on specified investments and payments.

Unlike salaried employees who automatically contribute to EPF through payroll, self-employed individuals need to actively plan their investments to utilise this deduction.

Options that qualify:

- Public Provident Fund (PPF): Government-backed long-term savings scheme with tax-free returns and a 15-year tenure. Often used by freelancers as a retirement planning tool.

- Equity Linked Savings Scheme (ELSS): Tax-saving mutual funds with a 3-year lock-in period (shortest in Section 80C instruments). These offer market-linked growth potential.

- Life insurance premiums: Premiums paid for policies covering yourself, your spouse, or children are eligible.

- National Savings Certificate (NSC): A fixed-income investment issued by post offices.

- 5-year tax-saving fixed deposits: Offered by banks and post offices. The principal qualifies for deduction while interest remains taxable.

- Children’s tuition fees: Tuition fees for up to two children’s full-time education in India.

- Principal repayment of home loan: Principal component of EMI payments can be claimed.

Additionally, contributions to a National Pension System (NPS) Tier I account qualify for an additional deduction of up to ₹50,000 under Section 80CCD(1B).

So, a self-employed individual can claim ₹2,00,000 in deductions through 80C and NPS combined.

Section 80D: Health Insurance Premiums

It allows deductions for health insurance premiums paid for yourself and your family.

For self-employed individuals who don’t have employer-provided medical coverage, this deduction is both financial protection and tax-saving.

The deduction limits depend on the age of the insured individuals.

| Coverage | Deduction Limit |

| Self, spouse, and dependent children (below 60 years) | Up to ₹25,000 |

| Parents below 60 years | Additional ₹25,000 |

| Parents aged 60 years or above | Additional ₹50,000 |

| Self or spouse aged 60 years or above | Up to ₹50,000 |

In certain cases, a self-employed individual supporting senior citizen parents can claim up to ₹1,00,000 per year under Section 80D.

In addition to this, preventive health check-ups up to ₹5,000 are also eligible within the overall deduction limit (e.g., within ₹25,000 for self/family or additional for parents).

Important requirements:

- Insurance premiums must be paid through non-cash methods such as bank transfer, card payment, or cheque.

- Cash payments are generally not eligible except for preventive health check-ups.

- Always retain policy documents and payment receipts for tax records.

Section 80E: Education Loan Interest Deduction

Provides a deduction for the interest component of education loan repayments (not the principal repayment). This benefit applies if the loan was taken for higher studies for:

- Yourself

- Your spouse

- Your children

- A student for whom you are the legal guardian

Unlike many other deductions, there is no upper limit on the amount of interest that can be claimed.

Conditions:

- Available for up to 8 consecutive assessment years starting from the year repayment begins.

- Loan must be taken from a recognised financial institution or approved charitable organisation. Loans from relatives or friends do not qualify.

- Courses must qualify as higher education, including professional or postgraduate programmes in India or abroad.

This deduction is especially valuable in the early years of repayment when the interest portion of the EMI is usually highest.

USING THE DEDUCTIONS

Sections 80C, 80D, and 80E together form a powerful tax planning toolkit for self-employed professionals.

When structured thoughtfully, they help you build long-term savings and retirement funds and reduce the tax burden on education loans

Example:

A freelancer investing ₹1.5 lakh under Section 80C, paying ₹25,000 in health insurance premiums, and claiming ₹50,000 in education loan interest could reduce taxable income by ₹2.25 lakh in a single financial year.

At the 30% tax bracket, that translates to a potential tax saving of ₹67,500 or more.

Home Office Deduction: How to Calculate

Many freelancers and independent professionals work from home, which is why home office deduction must be utilised properly.

Step 1: Confirm That Your Home Qualifies as a Workplace

Make sure your home functions as your primary place of business. For this, it should meet two conditions:

- Regular use: The area is used consistently for work activities such as client calls, design work, consulting sessions, writing, or administrative tasks.

- Defined workspace: There is a clearly identifiable area dedicated to work.

It doesn’t need to be a whole room, but it must be a consistent, clearly defined workspace, not a dining table used occasionally.

If you have a separate office elsewhere and only work from home occasionally, it’s harder to justify claiming a home office allocation.

Step 2: Identify the Expenses You Can Allocate

Once you establish eligibility, identify which household expenses can be partially claimed as business expenses.

Rent: For rented homes, rent is usually the largest deductible expense.

Utilities: Electricity, water, and similar bills can be claimed proportionately.

Internet/Broadband: Fully claimable if primarily for business; otherwise, you can claim the business-use portion.

Maintenance & Repairs: General expenses can be apportioned; workspace-specific repairs may be fully deductible.

For Homeowners: Rent isn’t claimable, but you can deduct a share of municipal taxes, maintenance charges, and depreciation on the business-use portion under Section 32.

Step 3: Calculate the Business-Use %age

The most defensible method for calculating the home office deduction is the area-based proportion method.

Business Use Percentage = (Workspace Area ÷ Total Carpet Area of Home) × 100

This percentage is then applied to eligible household expenses.

Example: A freelance consultant works from home with Total carpet area = 1,000 sq ft, and dedicated workspace = 150 sq ft

Business use percentage = 150 ÷ 1,000 = 15%

Monthly expenses:

- Rent = ₹30,000

- Electricity = ₹4,000

- Internet = ₹1,500

Deduction:

- Rent = 15% × ₹30,000 = ₹4,500/ month

- Electricity = 15% × ₹4,000 = ₹600/ month

Annual deduction from rent and electricity = (₹4,500 ×12) + (₹600×12) = ₹61,200/ year

This simple calculation can create ₹50,000 – ₹1,00,000 in annual deductions.

Step 4: Maintain Proper Documentation

Like all tax deductions, proper documentation is essential to support your claim:

- Rent agreement and rent payment records (bank transfers or receipts)

- Utility bills such as electricity and broadband

- Property tax receipts if you own the home

- Simple measurement record or floor plan showing workspace area vs total home area

The floor plan doesn’t have to be professionally drawn. Even a simple sketch with measurements can demonstrate that the deduction was calculated thoughtfully and consistently.

Depreciation on Assets: Laptops, Vehicles, Equipment

For self-employed tax payers, depreciation can become one of the most meaningful recurring deductions.

Depreciation is governed by Section 32 of the Income Tax Act, along with depreciation rates prescribed under the Income Tax Rules, 1962.

To claim depreciation:

- Asset must be owned by you

- Must be used for business or professional purposes

- Cost must be capital in nature, meaning the asset provides long-term value rather than being consumed within the year

Example: A designer investing in a high-performance laptop cannot expense the entire cost immediately. Instead, a portion of the cost is deducted each year as depreciation.

Written Down Value (WDV) Method & Depreciation Rates

Under this method, depreciation is applied to the remaining value of the asset each year. So, it’s higher in the early years and gradually decreases over time.

Depreciation Rates for Common Business Assets:

| Asset Type | Depreciation Rate (WDV) |

| Computers and laptops | 40% |

| Printers, scanners, computer peripherals | 40% |

| Mobile phones used for business | 15% |

| Motor cars (not used for hire) | 15% |

| Two-wheelers used for business | 15% |

| Office furniture and fittings | 10% |

| General plant and machinery | 15% |

| Cameras and professional equipment | 15% |

| Professional books | 40% |

| Intangible assets (software, licences, IP) | 25% |

Also, assets are grouped into blocks, and depreciation is calculated on the entire block rather than on individual items.

So, if you purchase a second laptop while already owning one used for business, both devices fall into the same “computer” asset block, and depreciation applies to the combined value.

Example: If a freelance developer purchases a laptop for ₹1,00,000, the depreciation deduction in the first year would be = 40% × ₹1,00,000 = ₹40,000

The remaining WDV becomes ₹60,000, and depreciation in the following year is calculated on that amount.

180-Day Rule for Depreciation

If an asset is used for business for 180 days or more during the financial year, you can claim full depreciation at the applicable rate.

If it is used for less than 180 days, only 50% of the depreciation rate is allowed in that year.

Example:

| Detail | Value |

| Laptop purchase price | ₹1,00,000 |

| Purchase date | 1 January |

| Depreciation rate | 40% |

| Allowed depreciation (Year 1) | 20% = ₹20,000 |

Remaining depreciation continues in later years based on the reduced value.

Vehicle Depreciation for the Self-Employed

Passenger vehicles used for business typically qualify for 15% annual depreciation.

For vehicles that serve both personal and professional purposes (as in most cases), only the business-use portion of depreciation and related expenses can be claimed.

Example:

- Vehicle cost: ₹8,00,000

- Depreciation rate: 15%

- Annual depreciation: ₹1,20,000

If the vehicle is used 60% for business, the deductible amount becomes = ₹1,20,000 × 60% = ₹72,000

The same percentage is applied to running costs including fuel, insurance, maintenance and servicing.

Required documentation:

- Purchase invoices showing date, vendor, and asset value

- Payment proof such as bank transfers or credit card statements

- A fixed asset register listing assets, cost, depreciation rate, and WDV each year

- Evidence of business usage where assets also serve personal purposes

Even a simple spreadsheet tracking assets and depreciation can make tax filing far easier.

Travel, Internet & Phone: Claiming Mixed-Use Expenses

Phone, internet connection, and travel costs as mixed-use expenses because they support both professional work and personal activities.

Deductions for such expenses are allowed only for the portion that relates to business use.

Internet and Broadband Expenses

Internet is a core business utility for many self-employed professionals. It’s used for client communication, online meetings, research, invoicing, and project delivery.

But, since most household connections are shared with family members, the correct approach is to estimate the business usage percentage.

- Predominantly work usage: Mainly used for professional tasks, claim 70 -80% of the bill

- Shared household connection: Used equally by family members, go for 50 -60% business allocation.

- Dedicated business connection: For a separate broadband line exclusively for work, 100% can be claimed.

Example: If your monthly internet bill is ₹1,200 and 70% of it is used for business, you can claim a deduction of ₹840 per month, which amounts to ₹10,080 in deductible expenses over a full year.

Maintain:

- Monthly service provider invoices

- Payment records (bank transfer, UPI, or card payment)

- Brief note explaining how the%age was estimated

Mobile Phone Expenses

Most professionals use the same device for both client communication and personal calls. There are two practical ways to handle this:

Dedicated business number: If you maintain a separate SIM card or phone used exclusively for work, the entire monthly bill can be claimed as a business expense.

Single phone for personal and business use: If one phone serves both purposes, apply a reasonable business-use%age, typically between 50 and 70%, depending on actual usage.

Example: If your monthly mobile bill is ₹900 and 60% is used for business, you can claim ₹540 per month as a deduction, which results in ₹6,480 of deductible expense annually

Mobile Device:

The cost of the mobile handset is treated as a capital asset and can be depreciated under Section 32, at 15% annually, based on the business-use proportion.

Accessories used exclusively for business purposes, such as headsets, microphones, or video call lighting equipment, may be claimed either as expenses or depreciated depending on their cost.

Travel Expenses for Business

These deductions are among the most scrutinised because the line between personal and professional travel can be unclear.

To qualify as a deduction, tour travel expenses must be incurred wholly and exclusively for business purposes:

- Travel for client meetings or project visits

- Attendance at industry conferences, seminars, or workshops

- Flights or train tickets for business trips

- Hotel accommodation during business travel

- Local transportation such as taxis, auto fares, or fuel for client visits

Travel costs that do not qualify:

- Personal vacations

- Travel between home and a fixed workplace (considered personal commuting)

- Family travel where business activities are incidental

Handling Trips That Combine Business and Personal Activities

Sometimes a trip includes both work and leisure. In such cases, only the portion related to business activities should be claimed.

Example:

| Trip Detail | Value |

| Total trip duration | 5 days |

| Business activities | 3 days |

| Personal days | 2 days |

| Total trip cost | ₹30,000 |

Deductible portion = 3 ÷ 5 × ₹30,000 = ₹18,000

The remaining ₹12,000 is treated as personal expenditure and should not be claimed.

For frequent business travel, make sure to gather a simple travel log like basic spreadsheet or note with key details:

- Date of travel & Destination

- Purpose of the trip (client meeting, conference, project visit)

- Mode of transport

- Amount spent

- Supporting reference such as meeting invitation or event registration

Over time, this record provides a clear timeline of tour business travel expenses.

Presumptive Taxation (44ADA): Flat 50% Deduction

Section 44ADA offers one of the simplest ways to calculate taxable income.

Instead of maintaining detailed books of accounts, tracking every expense, and preparing full financial statements, it allows you to declare 50% of your gross professional receipts as taxable income.

The remaining 50% is automatically treated as business expenses. You do not need to maintain receipts or documentation for those presumed expenses.

Eligibility for Section 44ADA

It applies specifically to resident professionals and partnership firms (excluding LLPs) engaged in certain professions notified under Section 44AA(1) of the Income Tax Act:

- Legal professionals: advocates and lawyers

- Medical practitioners: doctors and surgeons

- Engineers and engineering consultants

- Architects

- Chartered accountants and other accountants

- Technical consultants and IT professionals

- Interior decorators

- Film artists: actors, directors, and lyricists

- Company secretaries

- Authorised representatives

This covers a large number of modern freelance and independent professionals, especially in consulting, IT services, design, and specialised advisory roles.

Gross Receipts Limit for Eligibility

To opt for Section 44ADA, your gross professional receipts must not exceed ₹75 lakh in a financial year.

However, the higher limit applies only when 95% or more of receipts are received through banking channels such as UPI, NEFT, RTGS, or cheque.

This is how the limits works:

- Gross receipts ≤ ₹50 lakh: Eligible regardless of payment mode

- ≤ ₹75 lakh: Only if cash receipts ≤5% (i.e., ≥95% via banking channels like UPI, NEFT, cheque)

If your receipts exceed these limits, you cannot use Section 44ADA and must follow regular taxation.

How the 50% Presumptive Rule Works

Under Section 44ADA, it is presumed that half of your income is profit and the other half expenses.

So, you only pay tax on 50% of your gross receipts, regardless of the actual expenses you incur.

Example:

| Parameter | Amount |

| Gross professional receipts | ₹18,00,000 |

| Presumptive income (50%) | ₹9,00,000 |

| Chapter VI-A deductions (80C, 80D etc.) | ₹2,00,000 |

| Net taxable income | ₹7,00,000 |

A key advantage is that Chapter VI-A deductions such as Section 80C, 80D, and 80E can still be claimed after calculating presumptive income.

What is Your Income is More Than 50%

Section 44ADA sets a minimum profit threshold, not a maximum.

If your actual profit margin is higher than 50%, you are free to declare a higher amount. However, you cannot declare less than 50% unless you opt out of the presumptive scheme.

Example: If your receipts are ₹20 lakh but your real profit is closer to ₹16 lakh, you should ideally report a higher figure than the minimum presumptive income.

What You Cannot Claim Under 44ADA

Since it’s already assumed that 50% of receipts are expenses, you cannot claim additional business deductions like:

- Office rent or coworking expenses

- Internet and phone bills

- Travel expenses

- Depreciation on assets such as laptops or vehicles

- Staff salaries or contractor payments

- Home office deductions

These costs are considered to be already included in the presumed 50% expense allowance.

Advance Tax Rules Under Section 44ADA

Normally, taxpayers must pay advance tax in four installments during the financial year.

However, professionals opting for presumptive taxation can pay 100% of their advance tax liability in a single installment by 15 March.

This reduces compliance throughout the year.

| Choose Section 44ADA When | Choose Regular Taxation When |

| Expenses < 50% of receipts | Expenses > 50% of income |

| Prefer minimal bookkeeping | Large equipment/depreciation claims |

| Income within eligibility limit | High operating costs (rent, salaries) |

Health Insurance & NPS: Additional Tax Savings

Health insurance and NPS contributions address two major financial risks faced by self-employed individuals: unexpected medical costs and retirement planning without employer support.

Let’s take a look at the deductions available here:

Health Insurance Under Section 80D

Section 80D allows deductions for premiums paid for health insurance policies covering yourself, your family, and your parents.

The deduction limits can reach ₹1,00,000 per year depending on the age of the insured individuals and has been discussed above.

Example: Consider a freelance consultant aged 35 who pays:

- ₹24,000 annual premium for family coverage

- ₹48,000 annual premium for senior citizen parents

Total deduction = ₹24,000 + ₹48,000 = ₹72,000 deduction under Section 80D.

Preventive Health Check-ups

Section 80D allows up to ₹5,000 for preventive health check-ups for yourself, your spouse, children, or parents.

This amount is included within the overall limit, not in addition to it.

One advantage is that check-ups can be paid in cash, while insurance premiums must be paid through banking channels.

NPS Contributions and Additional Tax Benefits

The National Pension System (NPS) is one of the most tax-efficient retirement instruments for self-employed professionals.

There are two relevant deduction sections.

Section 80CCD(1): Within the Section 80C Limit

Contributions to an NPS Tier I account qualify for deduction under Section 80CCD(1).

For self-employed individuals, the maximum deduction allowed is up to 20 percent of gross total income, subject to the overall ₹1.5 lakh limit of Section 80C.

So, NPS contributions compete with other tax-saving investments such as PPF, ELSS mutual funds, life insurance premiums, and tuition fees.

Section 80CCD(1B): The Additional ₹50,000 Deduction

This provision allows an additional deduction of up to ₹50,000, over and above the ₹1.5 lakh Section 80C limit.

This raises the total deduction potential to ₹2,00,000 from investments alone.

How NPS Works for Self-Employed Professionals

Most major banks and financial platforms allow you to open a Tier I NPS account online.

- Contributions can be made at any time during the year

- Minimum annual contribution is ₹1,000

- Investments are allocated across equities, corporate bonds, and government securities

- Asset allocation can be chosen based on risk preference

Combining 80D and NPS to Maximize Tax Savings

When used together with Section 80C investments, health insurance and NPS contributions can significantly increase total deductions.

| Deduction Section | Maximum Amount |

| Section 80C investments | ₹1,50,000 |

| NPS additional deduction (80CCD(1B)) | ₹50,000 |

| Health insurance (self and family) | ₹25,000 |

| Health insurance for senior citizen parents | ₹50,000 |

| Total potential deduction | ₹2,75,000 |

NOTE:

Remember that deductions under Sections 80D and 80CCD(1B) are available only under the old tax regime.

If you opt for the new tax regime under Section 115BAC, these deductions are generally not permitted.

Record-Keeping Best Practices for Self-Employed

Documentation makes every tax claim defensible. Without this evidence, deductions you claim may not withstand scrutiny.

Here are some best practices to adopt as self employed:

Understand Your Record-Keeping Obligations

The level of documentation you need partly depends on your taxation method.

If you use presumptive taxation under Section 44ADA, you don’t have to maintain full books of accounts, but you should still be able to prove your gross receipts if asked.

If you opt for regular taxation, maintain proper books as it is a legal requirement and necessary to support expense deductions.

Either way, some records are essential to keep.

Track Every Income Record

Every payment you receive should be traceable through invoices and bank records, including

- Client invoices with sequential numbers and dates

- Bank statements showing incoming payments

- Payment platform records (Razorpay, PayPal, UPI apps)

- Form 26AS and AIS to verify TDS entries

- TDS certificates (Form 16A) from clients

Reconcile your invoices with bank deposits each month so your reported income matches your tax records.

Keep All Expense Records

If you claim business deductions, each expense should be backed by documentation, an invoice or receipt along with proof of payment.

| Expense Category | Records to Maintain |

| Office rent | Rent agreement and payment receipts |

| Utilities | Electricity, phone, and internet bills |

| Professional services | Invoices from accountants, lawyers, or consultants |

| Software subscriptions | Email invoices or payment confirmations |

| Travel expenses | Tickets, hotel invoices, and transport receipts |

| Equipment purchases | Purchase invoices for laptops, cameras, or furniture |

| Advertising and marketing | Platform invoices from Google Ads or social media |

Organise expenses by category within each financial year to simplify tax filing and reduce risk of losing documents.

Asset Register for Depreciation

If you claim depreciation under Section 32, it’s important to maintain an asset register. Keep a simple spreadsheet that includes:

- Asset description

- Purchase date

- Purchase cost

- Applicable depreciation rate

- Opening and closing written down value (WDV)

- Depreciation claimed each year

The record ensures you can calculate depreciation correctly and track assets throughout their useful life.

Client Agreements and Contracts

Invoices show what was billed, but contracts explain the work performed. Keeping agreements or engagement letters helps establish your professional relationship with clients.

They help:

- Show the relationship is professional, not employment

- Define payment terms and project scope

- Explain large or irregular payments

Even simple email confirmations outlining project terms can serve as useful records.

GST Records (If Applicable)

If your annual turnover exceeds ₹20 lakh for services, GST registration becomes mandatory. Once registered, maintaining GST records becomes essential for compliance.

Documents needed:

- Sales register containing all GST invoices

- Purchase register for expenses with input tax credit

- Copies of GST returns such as GSTR-1 and GSTR-3B

- GST payment challans and acknowledgements

How Long Should You Keep the Records?

| Record Type | Recommended Retention Period |

| General tax and business records | 6 years after the assessment year |

| Asset purchase records | Until disposal plus 6 years |

| GST records | 5 years from annual return due date |

| TDS certificates | At least 6 years |

When in doubt, keeping records longer is usually safer and easier than reconstructing missing information later.

Digital Record-Keeping

Digital systems reduce the risk of lost documents and make organisation easier. Helpful practices:

- Use accounting tools like Zoho Books, Tally, or QuickBooks

- Keep a dedicated business bank account for separate transactions

- Scan receipts immediately with mobile apps

- Organise files by financial year and expense category

Cloud storage like Google Drive or Dropbox also makes documents easy to retrieve if needed.

Monthly Reconciliation

One of the biggest mistakes self-employed professionals make is waiting until the end of the financial year to organise their finances.

Instead, reviewing records once a month helps ensure:

- All invoices have been issued and recorded

- Expenses are properly documented

- Bank transactions match your records

This habit prevents the stressful process of reconstructing an entire year of finances during tax season.