Expert verified

Expert verified Written By – PKC Desk, Edited By Karunakaran, Reviewed By – Aakash

TL;DR SummaryPartnership firms in India have significant tax-saving opportunities — from optimizing partner remuneration and claiming interest deductions to leveraging depreciation, R&D benefits, and the presumptive taxation scheme under Section 44AD. This guide walks through 17 practical, legally compliant tax hacks that help Indian partnership firms reduce their tax burden while staying fully compliant with the Income Tax Act. Whether you are a traditional partnership or an LLP, the right structure, proper bookkeeping, and professional tax advisory can make a measurable difference to your firm’s bottom line. |

Partnership firms in India can legally reduce their tax burden by maximising partner remuneration within Section 40(b) limits (up to 90% of book profit on the first ₹3 lakh, 60% on the balance), claiming interest on partner capital at up to 12% per annum, deducting rent paid to partners for premises, and leveraging depreciation, R&D benefits, and Section 80D health insurance premiums.

Firms with turnover up to ₹2–3 crore can further simplify compliance and reduce tax burden by opting for the presumptive taxation scheme under Section 44AD (6–8% of turnover), while those with higher turnover should evaluate converting to an LLP for structural tax advantages and limited liability.

Want to keep more of your hard-earned profits? Learn simple yet effective tips on how to save tax in partnership firm in India.

We take you through some of the most useful tax-saving opportunities that can help you minimize your tax burden as an Indian partnership firm.

Save More, Pay Less: Tax Tips for Indian Partnership Firms

By strategically implementing the following tax-saving measures, a partnership firm in India can effectively reduce its tax liability while remaining compliant with tax laws:

1.Optimize Partner Remuneration:

Partners’ remuneration, such as salary, bonus, or commission, is a deductible expense for the firm. Properly structuring it can significantly reduce the firm’s tax liability.

The remuneration, however, must comply with the limits set under the Income Tax Act, which is based on the book profits of the firm.

Under Section 40(b) of the Income Tax Act 1961 (renumbered to Section 35(e) of the Income Tax Act 2025) remuneration paid to working partners is allowed as a deduction subject to prescribed limits based on book profits.

|

Book Profit |

Maximum Allowable Remuneration |

|

On first ₹3,00,000 of book profit or in case of loss |

Higher of ₹1,50,000 or 90% of book profit |

|

On balance book profit above ₹3,00,000 |

60% of such balance profit |

This provision helps partnership firms legally reduce taxable income by compensating working partners through salary, bonus, commission, or remuneration.

To claim this deduction:

- The remuneration must be authorized by the partnership deed.

- The payment should be made only to working partners.

- The amount should remain within the limits prescribed under Section 40(b)

2.Claim Deduction on Interest:

Partners can receive interest on their capital contributions, and the firm can claim a deduction for this interest.

The interest should not exceed 12% per annum as per the Income Tax Act. Ensure that the interest rate is within this limit to allow the firm to reduce taxable income.

3. Make Use of Rent and Other Allowances:

If a partner provides premises or assets for the firm’s use, the rent or lease amount paid by the firm can be claimed as a deduction.

This reduces the taxable income while compensating the partner for their contribution.

4. Consider Tax-Efficient Partnership Structure:

Choosing the right partnership structure is essential for tax efficiency.

For instance, an LLP (Limited Liability Partnership) may offer benefits like no dividend distribution tax and simpler compliance, which can lead to tax savings compared to a traditional partnership firm.

Choosing between a traditional partnership firm and a Limited Liability Partnership (LLP) can significantly impact taxation, compliance requirements, and operational flexibility. Below, we have provided a comparison table between an LLP and a Partnership Firm.

|

Particulars

|

Partnership Firm |

LLP |

|

Governing Law |

Indian Partnership Act, 1932 |

LLP Act, 2008 |

|

Separate Legal Entity |

No |

Yes |

|

Liability of Partners |

Unlimited |

Limited Liability |

|

Tax Rate |

30% |

30% |

|

Surcharge Applicability |

12% above ₹1 crore |

12% above ₹1 crore |

|

Alternate Minimum Tax (AMT) |

Not Applicable |

Applicable under certain conditions |

|

Tax Audit Applicability |

Section 44AB applicable |

Section 44AB applicable |

|

Presumptive Taxation (Section 44AD) |

Eligible subject to conditions |

LLPs are generally not eligible |

|

ROC/MCA Compliance |

Minimal |

Mandatory annual MCA filings |

5.Seek Professional Advice :

Hiring a tax professional from trusted firms like PKC Management Consulting can help in identifying specific deductions and credits that the firm might otherwise miss. Explore our comprehensive Tax Advisory Services to see how our experts help partnership firms across India structure their finances for maximum tax efficiency while staying fully compliant with the Income Tax Act.

A tax expert can provide advice that is customized to your firm’s unique circumstances, ensuring compliance while optimizing tax savings.

6.Explore Tax Benefits for Women Entrepreneurs

If the partnership firm is led by women, it may qualify for specific government schemes and incentives.

These schemes are aimed at promoting women’s entrepreneurship, which can include tax benefits.

Take the first step towards lower taxes. Book a FREE 30-minute consultation with PKC’s tax experts today — and get a personalized tax-saving plan built specifically around your partnership firm’s structure, profits, and compliance requirements.

7.Proper Planning of Partners’ Structure

By hiring family members as employees and paying them salaries, partnership firms can utilize the lower tax brackets for individuals.

Additionally, including non-resident partners can potentially benefit from lower tax rates or exemptions in their countries.

By hiring family members as employees and paying them salaries, partnership firms can utilize the lower tax brackets for individuals. Additionally, including non-resident partners can potentially benefit from lower tax rates or exemptions in their countries. For partners looking to further reduce personal tax exposure, also read: How to Save Capital Gain Tax on Sale of Shares — a practical guide to minimizing tax on investment profits

8.Take Advantage of Startup Deductions

If the partnership firm is a startup, it may be eligible for various deductions under the Income Tax Act.

These include deductions on expenses incurred before starting the business, as well as specific startup-related tax exemptions.

9.Leverage Research and Development (R&D) Benefits

Firms involved in R&D activities can claim deductions for expenses incurred on R&D, which can significantly reduce taxable income.

There are also additional benefits under Section 35 of the Income Tax Act for scientific research.

10.Capitalize on Export Promotion Incentives

Partnership firms engaged in export activities can avail of various government incentives.

These include duty drawback, export promotion capital goods (EPCG) scheme, and other incentives which can lead to substantial tax savings.

11.Utilize Investment Tax Credits:

Certain investments may qualify for tax credits, which can directly reduce the tax liability.

This includes investments in renewable energy projects or other government-specified sectors.

12.Look into Tax-Saving Investments

Partners can invest in tax-saving instruments like PPF, NSC, ELSS, etc., under Section 80C, which helps in reducing personal tax liability.

Additionally, the partnership firm can also invest in tax-saving bonds to reduce taxable income.

13.Utilize Depreciation on Business Assets:

The firm can claim depreciation on business assets, which is a non-cash expense.

This reduces the taxable income and allows for the deferred payment of taxes over the asset’s useful life.

14.Adopt Flexible Profit Distribution:

The partnership agreement should allow for flexible profit distribution based on the partners’ current tax situation.

Adjusting profit shares can help in optimizing overall tax liability, especially if partners are in different tax brackets.

15.Health Insurance Premiums

Partnerships can claim deductions for premiums paid on health insurance policies for partners and their families under Section 80D.

This can help in reducing taxable income.

16. Presumptive Taxation Scheme

Eligible partnership firms can opt for the presumptive taxation scheme under Section 44AD of Income Tax Act 1961 (Renumbered to Section 58 of Income Tax Act 2025) to simplify tax compliance and reduce accounting burden.

Key Conditions:

- Applicable for businesses with turnover up to ₹2 crore or ₹3 crore (subject to prescribed digital receipt conditions).

- Income is presumed at:

- 8% of turnover for cash receipts

- 6% of turnover for digital receipts

Benefits:

- Simplified tax calculation

- Reduced compliance burden

- No need to maintain detailed books of accounts under certain conditions

- Tax audit may not be required if conditions are satisfied

However, firms opting for presumptive taxation should carefully evaluate whether declaring income at the prescribed rates is beneficial compared to actual profit margins.

17. Maintain Proper Books & Accounts

Proper bookkeeping and accounting practices are essential to claim all eligible deductions and avoid penalties.

Accurate records ensure that the firm is compliant with tax laws and can substantiate claims during assessments.

When is Tax Audit Mandatory for a Partnership Firm?

A partnership firm is required to get its accounts audited under Section 44AB of Income Tax Act, 1961 (renumbered to Section 63 of the Income Tax Act, 2025) in the following cases:

|

Situation |

Tax Audit Requirement |

|

Business turnover exceeds ₹1 crore |

Tax audit mandatory |

|

Business turnover up to ₹10 crore where cash receipts and cash payments exceed 5% of total receipts/payments |

Tax audit mandatory if cash transactions exceed prescribed limit |

|

Professional gross receipts exceed ₹50 lakh |

Tax audit mandatory |

|

Firm opts for presumptive taxation and declares income lower than prescribed limits |

Tax audit may become mandatory |

|

Firm eligible under presumptive taxation but fails to satisfy conditions of the scheme |

Audit applicable subject to prescribed income criteria |

Professional Tax Advisory Can Help Optimize Savings

Tax planning for partnership firms involves much more than simply filing returns. Proper structuring of partner remuneration, interest on capital, depreciation claims, presumptive taxation eligibility, and audit compliance can collectively result in substantial tax savings.

Explore our professional Tax Advisory Services to understand how strategic tax planning can improve compliance while legally reducing tax liability for your partnership firm.

Frequently Asked Questions About Tax Saving for Partnership Firms

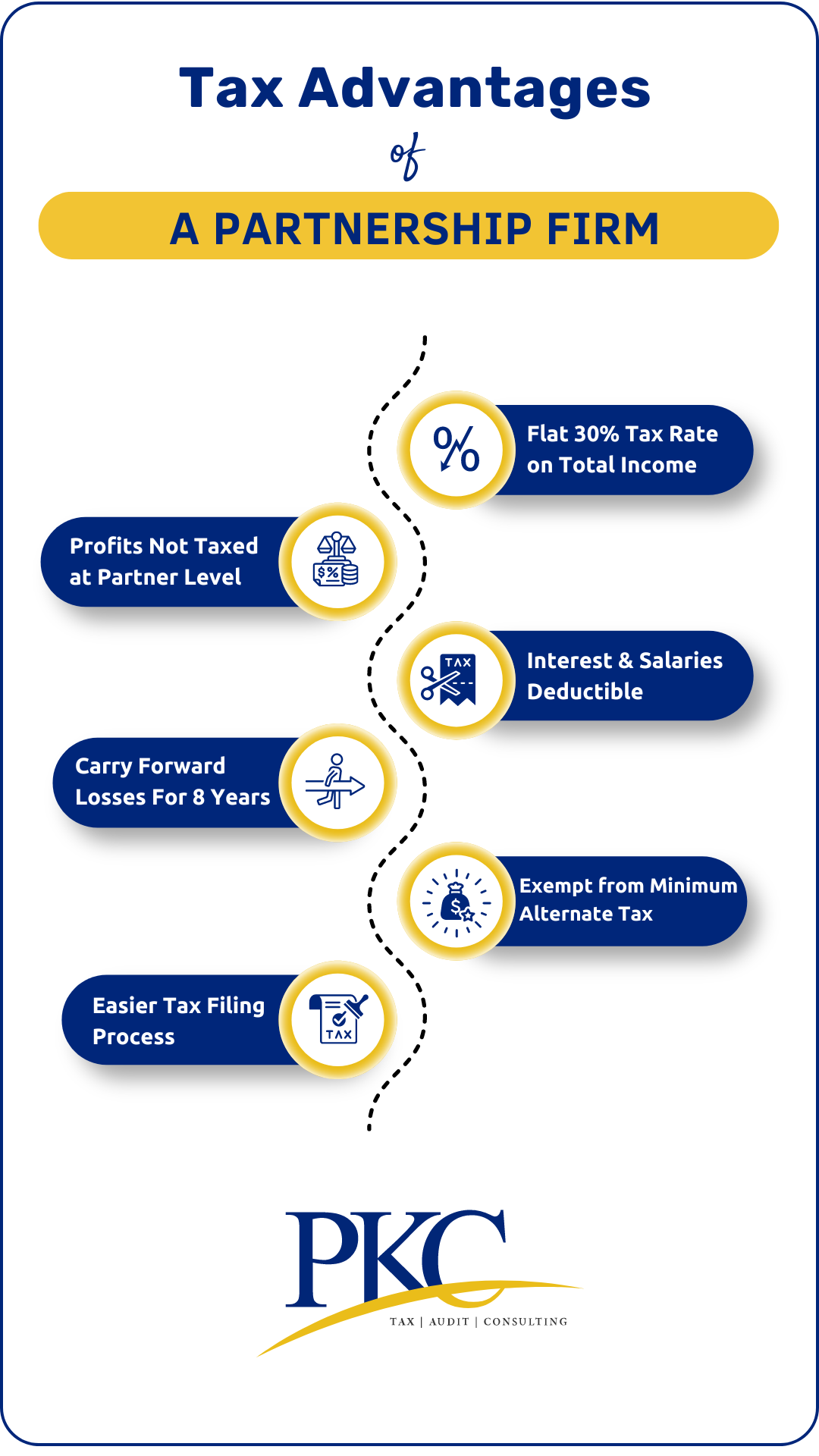

Partnership firms are not subject to Minimum Alternate Tax (MAT), and they benefit from pass-through taxation. This means profits and losses are passed through to the individual partners, who are taxed on their share.

A partnership firm can maximize deductions by claiming deductions for interest on capital, partner remuneration, rent, depreciation, and donations.

Partnership firms can invest in eligible instruments like PPF, ELSS, and life insurance policies to claim deductions under Section 80C, 80D, and 80G of the Income Tax Act.

Yes, partnership firms can consider converting to an LLP or one person company (OPC) if it suits their business needs and offers potential tax advantages.

By maintaining detailed and organized records of all business transactions, partnership firms can support their tax claims and avoid penalties.