Expert verified

Expert verified Top Tips for Saving Tax on Sale of Gold in India

In order to save tax on sale of gold in India, you can adopt the following strategies

1.

Assess Holding Period Tax Implications:

If possible choose the time for which you are holding gold based on the tax implications.

Compare STCG (taxed at individual tax slabs) with LTCG (taxed at 12.5%) and choose the one that minimizes your tax liability.

2.

Utilize Tax-Loss Harvesting:

This involves selling other investments that you have incurred losses on to offset the capital gains from the sale of gold.

Time the sale of underperforming assets and reduce their overall taxable income. This can help lower capital gains tax on their gold transactions.

3.

Consult a Tax Professional:

A trusted tax consultant can help you structure the sale of gold in the most tax-efficient manner. PKC’s Tax Advisory Services cover capital gains planning, reinvestment structuring, and ITR filing — so you don’t leave exemptions on the table.

Since they stay up to date with the financial regulations, they help you optimize your tax liability by structuring the sale of gold in the most tax-efficient manner.

4.

Claim Exemption for Residential Property

Under Section 54F of the Income Tax Act, if you reinvest the gains from selling gold into residential property, you can claim an exemption on capital gains. The same Section 54F logic applies when selling commercial property — if you’re exploring that route, our detailed guide on How to Save Tax on Sale of Commercial Property walks through the full reinvestment conditions and 11 tax-saving options.

However, make sure you do it within a specified period, which currently is one year before or two years after the sale.

5.

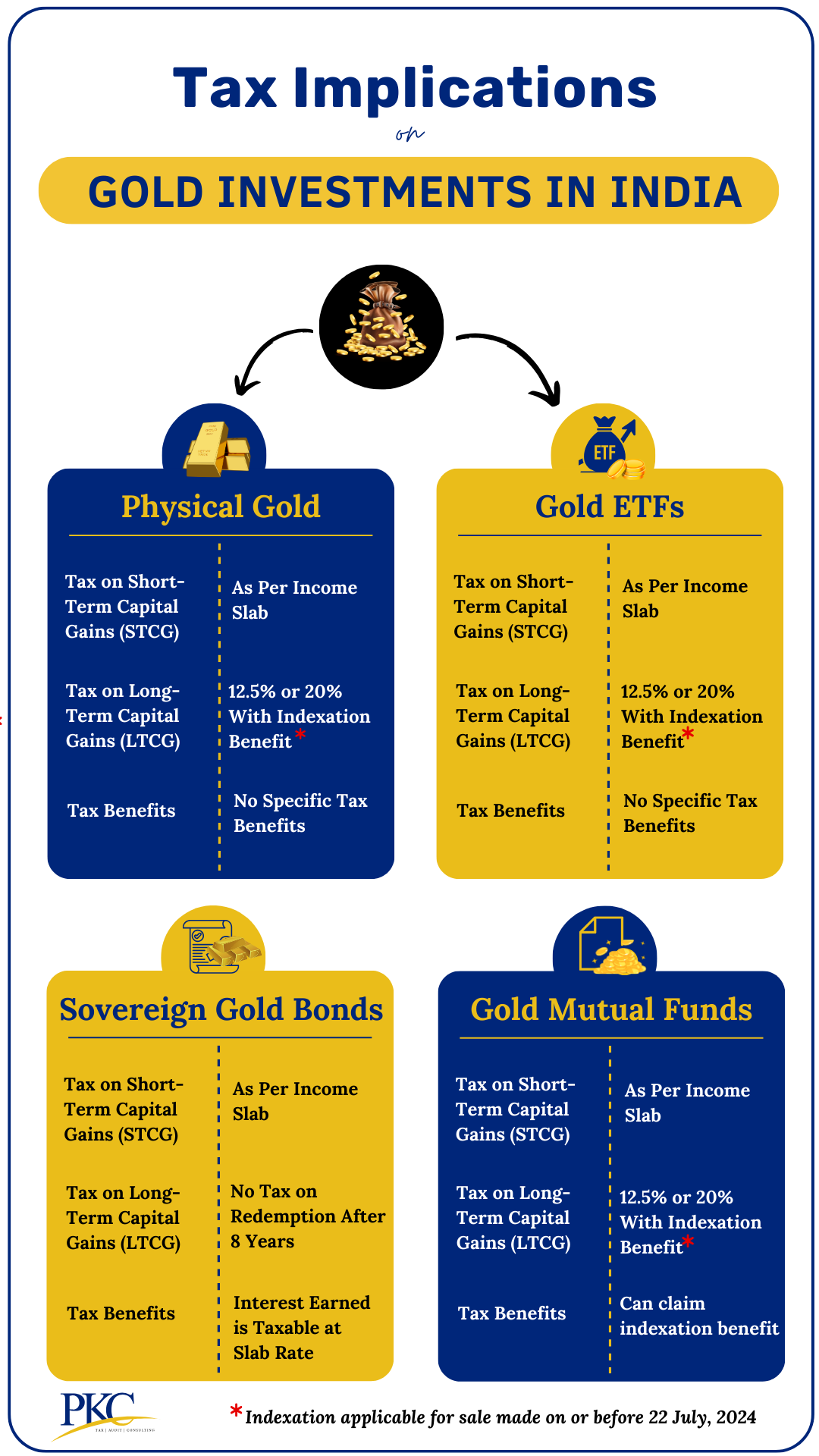

Sovereign Gold Bond (SGB)

Sovereign Gold Bonds offer one of the most tax-efficient routes to gold investment in India. If you hold SGBs until maturity (8 years), the capital gains on redemption are completely exempt from tax — making them significantly more advantageous than physical or digital gold.

However, if you sell or transfer your SGBs on the exchange before maturity, the gains are taxed just like physical gold. This means LTCG at 12.5% if held for more than 24 months, or at your applicable slab rate if held for 24 months or less.

Note that the 2.5% annual interest earned on Sovereign Gold Bonds (SGBs) is taxable as per your income tax slab, irrespective of when you redeem the bonds. If your objective is a long-term, tax-efficient investment in gold, holding SGBs until maturity continues to be the most beneficial option available.

6.

Digital Gold — Same Tax Rules as Physical Gold

Many investors today buy gold through apps like PhonePe, Paytm, or MMTC-PAMP, assuming digital gold may be treated differently for tax purposes. It is not. Digital gold carries exactly the same tax treatment as physical gold — STCG at your slab rate if sold within 24 months, and LTCG at 12.5% if held beyond 24 months, with no indexation benefit.

Unlike Sovereign Gold Bonds, digital gold offers no maturity-based exemption. It is therefore important to track your purchase date carefully and retain all transaction records and receipts from the platform, as these serve as proof of your cost of acquisition when computing capital gains.

7.

Consider Gold Loans

Instead of selling gold, consider taking a loan against your gold assets.

This strategy also ensures that you retain ownership of your gold while obtaining funds for immediate needs without incurring capital gains taxes.

8.

Invest in Government Specified Bonds

Consider investing in specified government bonds, which allows individuals to claim exemptions on long-term capital gains.

The investment must be made within six months into entities like the National Highway Authority of India and Rural Electrification Corporation.

9.

Capital Gains Account Scheme (CGAS)

If you plan to reinvest the sale proceeds, but need more time, you can deposit the gains into a Capital Gains Account Scheme (CGAS) to temporarily save the tax.

This keeps the exemption intact as long as you reinvest the amount within the allowed timeframe.

10.

Make Use of the Inheritance Clause

If gold is inherited, the capital gains tax is calculated based on the original purchase price by the person who bought the gold.

The holding period is also counted from the original date of purchase. This could help classify it as a long-term asset and reduce your tax burden.

Inherited assets follow similar cost-of-acquisition rules across the board — if you’ve also inherited property and are planning a sale, see our guide on How to Save Tax on Sale of Ancestral Property for strategies specific to that scenario

11.

Plan Sales Strategically

Timing the sale of gold can help you save taxes. For instance, if you expect to fall into a lower tax bracket in the next financial year, consider delaying the sale until then.

Alternatively, you can spread out the sale over different financial years to avoid a high tax slab.

12.

Special Provisions for Senior Citizens

In some cases, senior citizens may benefit from lower tax rates or exemptions on capital gains derived from selling gold.

Understanding these provisions can improve your financial planning and reduce overall tax burdens for older individuals.

13.

Gift or Transfer

You can gift or transfer gold to family members, particularly those in lower tax brackets, or through inheritance.

Gifting gold to relatives is not taxable, and when they sell it, the tax will be calculated based on their income bracket, potentially resulting in lower taxes.

14.

GST on Gold

Beyond capital gains tax, it is important to understand how GST affects your overall cost when buying gold. A 3% GST applies on gold coins, bars, and jewellery, and an additional 5% GST is levied on making charges for jewellery. When you sell gold back to a jeweller or dealer, GST is generally not applicable on your side — the buyer accounts for it.

One common misconception is that GST paid at the time of purchase can be offset against your capital gains tax liability. These are two separate tax regimes, and no such deduction is available. Similarly, GST paid does not increase your cost of acquisition for capital gains purposes — only the documented gold value and associated charges factor into that calculation.

15.

Sell Gold Through Recognized Jewellers

Although not a direct answer to how to save tax on sale of gold jewellery, this can make a significant impact.

Selling gold through recognized jewellers can provide documentation and transparency in transactions.

This helps with establishing the purchase price and any additional costs associated with the gold, which can be deducted from the selling price to calculate capital gains accurately.