Introduction

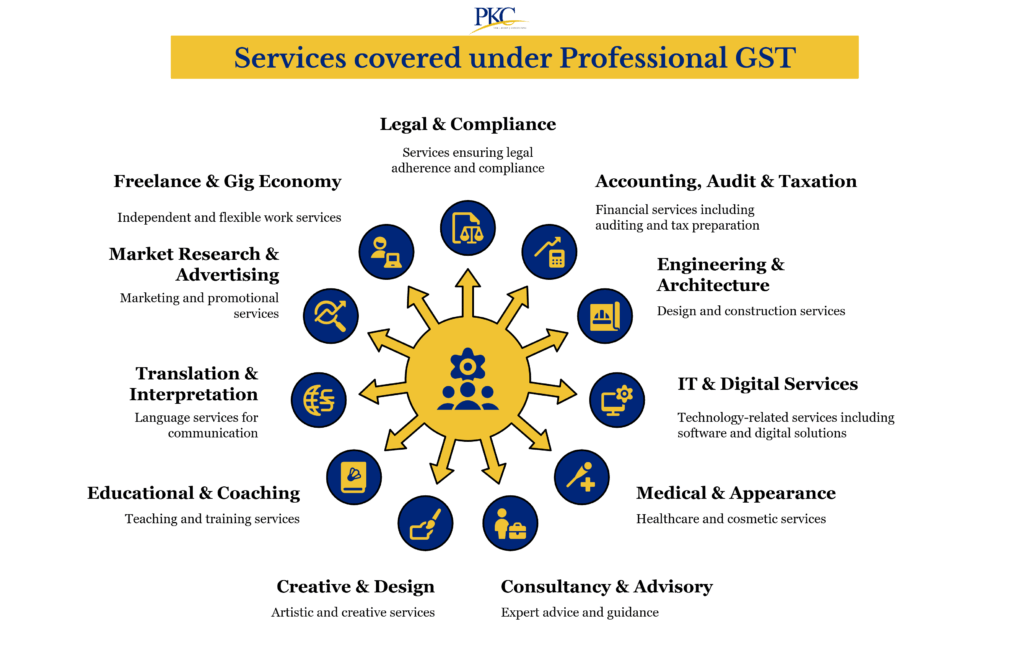

Goods and Services Tax (GST) has changed the taxation system for service providers in India. Professionals such as Chartered Accountants, lawyers, consultants, architects, engineers, doctors, freelancers, management advisors, designers, and technology consultants are now required to understand GST compliance carefully.

Many professionals still have practical doubts about GST registration, invoicing, reverse charge mechanism (RCM), input tax credit (ITC), e-invoicing, TDS provisions, and filing requirements. Incorrect GST compliance may lead to notices, penalties, delayed refunds, and tax disputes.

This updated guide explains GST for professional services in simple language for business owners, consultants, freelancers, and professional firms. The article also includes the latest 2026 updates relating to e-invoicing, reverse charge mechanism, and the new TDS Section 393 framework under the Income Tax Act, 2025.

This article is prepared for the website of PKC India, a professional services firm providing taxation, audit, advisory, and compliance services to businesses across India.

r Professional Services?

GST for professional services refers to the tax applicable on services provided by professionals and consultants. Under GST law, services provided for consideration during the course or furtherance of business are generally taxable unless specifically exempted.

Professional services may include:

- Chartered Accountancy services

• Legal services

• Consultancy services

• Technical advisory

• Engineering services

• Architectural services

• Interior design services

• Digital marketing consultancy

• Financial advisory

• IT consultancy

• Business management services

• Freelancing services

Most professional services attract GST at 18%, unless specifically exempted under law.

Who is Considered a Professional Under GST?

The GST law does not provide a single comprehensive definition for “professional services.” In practice, professional services generally refer to specialised services provided based on qualification, expertise, training, or technical knowledge.

Professionals may operate as:

- Proprietorship firms

• Partnership firms

• LLPs

• Private limited companies

• Independent freelancers

GST applicability depends on the nature of services and turnover thresholds.

GST Registration Threshold for Professional Services

One of the most important questions asked by consultants and professionals is whether GST registration is mandatory.

Under GST law, service providers are generally required to obtain GST registration if aggregate turnover exceeds:

- ₹20 lakh in a financial year for normal category states

• ₹10 lakh in a financial year for special category states

Special category states generally include certain North-Eastern and hill states as notified under GST law.

Aggregate turnover includes:

- Taxable services

• Exempt services

• Export services

• Interstate supplies

The threshold applies on an all-India basis under the same PAN.

When GST Registration Becomes Mandatory Even Below Threshold

Certain situations may require GST registration even if turnover is below ₹20 lakh.

Examples include:

- Interstate taxable supplies in specified situations

• E-commerce operator-related services in certain cases

• Reverse charge applicability

• Voluntary registration

• Input tax credit planning

• Requirement by clients or contracts

Professionals should evaluate registration applicability carefully before assuming exemption.

GST Rate for Professional Services

Most professional services are taxable at 18% GST.

This usually consists of:

- 9% CGST + 9% SGST for intra-state services

OR

• 18% IGST for interstate services

Examples of services generally taxable at 18%:

- CA services

• Legal consultancy by law firms

• Management consultancy

• Engineering consultancy

• IT consultancy

• Recruitment consultancy

• Interior design services

• Marketing consultancy

However, some services may be exempt under specific notifications.

GST Exemptions for Certain Professional Services

Certain professional services may enjoy GST exemption subject to conditions.

Examples may include:

- Healthcare services by clinical establishments and authorized medical practitioners

• Certain educational services

• Services provided by advocates to non-business entities in specified cases

• Agricultural extension services in specified cases

Exemptions depend on the exact nature of services and recipient category. Professionals should verify exemption notifications carefully before treating services as exempt.

Time of Supply for Professional Services

Under GST, tax liability generally arises at the earlier of:

- Date of invoice

OR

• Date of payment

Professionals should issue invoices within prescribed timelines to avoid compliance issues.

For continuous or long-term consultancy assignments, contract terms and milestone-based billing should be properly documented.

Place of Supply for Professional Services

Determining the place of supply is important because it affects whether CGST-SGST or IGST is charged.

For most B2B professional services:

Place of supply is generally the location of the registered recipient.

For B2C services:

Place of supply may depend on the location of the recipient or supplier based on the nature of services.

Incorrect place of supply determination may result in wrong tax payment and future disputes. For a detailed breakdown of how place of supply determines whether CGST+SGST or IGST applies to your invoices, read our complete guide on CGST vs SGST vs IGST.

GST Invoice Requirements for Professional Services

A GST invoice for professional services generally contains:

- Name and address of supplier

• GSTIN

• Invoice number and date

• Client details

• Description of services

• SAC code

• Taxable value

• GST rate and tax amount

• Place of supply

• Signature or digital authentication

Professionals should maintain proper invoice numbering and documentation systems.

SAC Code for Professional Services

SAC stands for Services Accounting Code.

Different professional services fall under different SAC classifications.

Examples:

- Accounting and auditing services

• Legal services

• Architectural services

• Information technology consultancy services

• Management consultancy services

Using the correct SAC code helps proper GST reporting.

Input Tax Credit (ITC) for Professional Services

Input Tax Credit is one of the most important benefits under GST.

Professionals can generally claim ITC on GST paid for business-related expenses used in the course of providing taxable services.

Examples where ITC may generally be available:

- Office rent

• Professional software subscriptions

• Internet expenses

• Office equipment

• Audit and consultancy expenses

• Business travel expenses

• Staff training expenses

• Telephone and communication expenses

However, ITC is subject to conditions and restrictions under GST law.

ITC Eligibility Table for Professional Services

Eligible for ITC

- Office rent used for business

• Laptop and computer purchases

• Accounting software

• Professional subscriptions

• Internet and telephone bills

• Office stationery

• Consultancy services received

• GST paid on business travel subject to conditions

Generally Restricted or Blocked ITC

- Personal expenses

• Motor vehicles in many cases

• Club memberships

• Food and beverages in many cases

• Personal travel expenses

• Employee-related personal consumption

• Expenses without proper GST invoices

Professionals should maintain proper documentation and vendor GST compliance checks before claiming ITC.

Composition Scheme for Professionals

Earlier, professionals had limited applicability under composition schemes. Over time, GST law introduced composition options for certain service providers subject to turnover conditions.

Professionals considering composition schemes should evaluate:

- Reduced compliance benefits

• Restrictions on ITC

• Restrictions on interstate supplies in certain cases

• Lower tax rates

• Client expectations regarding GST invoices

The decision should be based on business model and customer profile.

GST Returns Applicable to Professionals

Professionals registered under GST may be required to file:

- GSTR-1

• GSTR-3B

• Annual return in applicable cases

The return frequency may depend on turnover and the selected filing scheme.

Timely filing is important because delayed returns may result in:

- Late fees

• Interest liability

• ITC blockage

• Compliance notices

E-Invoicing for Professional Services Firms — Mandatory from ₹5Cr Turnover

E-invoicing has become an important compliance requirement under GST.

As applicable in 2026, businesses crossing prescribed turnover thresholds are required to generate e-invoices through the Invoice Registration Portal (IRP).

Professional services firms with aggregate turnover exceeding ₹5 crore are required to comply with e-invoicing requirements, subject to applicable GST notifications and amendments.

Under e-invoicing:

- Invoice data is uploaded to the IRP

• Invoice Reference Number (IRN) is generated

• QR code is generated

• Invoice becomes GST-compliant for reporting purposes

Applicability is determined based on aggregate turnover in preceding financial years.

Why E-Invoicing is Important for Professionals

E-invoicing helps:

- Reduce invoice mismatches

• Improve GST reporting accuracy

• Reduce fake invoice risks

• Simplify reconciliation

• Improve compliance tracking

Professional firms should ensure their accounting software is compatible with IRP integration requirements.

Consequences of Non-Compliance with E-Invoicing

If e-invoicing is applicable but invoices are not generated through the prescribed system:

- Invoice may be treated as invalid

• ITC issues may arise for clients

• GST penalties may apply

• Compliance notices may be issued

Therefore, firms crossing turnover thresholds should review applicability carefully.

What is RCM Under GST for Professional Services — Updated 2026 List

Reverse Charge Mechanism (RCM) means GST liability shifts from the supplier to the recipient in specified cases.

Certain professional services continue to fall under RCM in 2026.

Examples generally covered under RCM include:

- Legal Services by Advocates

Services provided by an advocate or firm of advocates to a business entity are generally covered under reverse charge subject to applicable conditions.

- Director Services

Services provided by directors to companies are generally covered under reverse charge under GST.

- Certain Services by Chartered Accountants and Professionals

Most CA services are generally taxed under forward charge. However, businesses should evaluate specific transactions carefully for RCM applicability wherever notified.

- Sponsorship Services

Certain sponsorship-related transactions may fall under RCM.

- Import of Services

Import of professional services may require GST payment under reverse charge.

Businesses receiving services under RCM must:

- Pay GST directly

• Report liability properly

• Maintain documentation

• Claim ITC subject to eligibility

Professionals should regularly review updated RCM notifications because applicability may change through amendments and clarifications.

New TDS Section 393 — What Changed from April 2026

From 1 April 2026, the Income Tax Act, 2025 introduced structural changes in TDS provisions.

The earlier TDS framework under Section 194J of the Income-tax Act, 1961 has now been reorganized under Section 393 of the Income Tax Act, 2025 for specified non-salary payments. citeturn0search0turn0search3turn0search12

The objective of the new structure is simplification and consolidation of TDS provisions.

Key practical points for professional services:

- Professional fees continue to attract TDS provisions

• Reporting structure has changed under the new Act

• Section references in returns and certificates may change

• Businesses should update accounting and ERP systems accordingly

As per available guidance and mapping documents, the old Section 194J references relating to professional fees have been mapped into Section 393 structures under the Income Tax Act, 2025. citeturn0search1turn0search3turn0search12turn0search13

Businesses and professionals should consult tax advisors for updated compliance procedures under the new framework.

GST Compliance Checklist for CA Firms and Consultants

Professional firms should maintain a practical GST compliance process.

Basic GST Checklist

Registration

- Verify GST registration applicability

• Update principal place of business

• Review additional place registrations

Invoicing

- Use correct GST rates

• Mention SAC codes

• Verify client GSTIN

• Generate e-invoice where applicable

Returns

- File GSTR-1 on time

• File GSTR-3B on time

• Reconcile turnover periodically

ITC Review

- Match vendor invoices

• Reconcile GSTR-2B

• Review blocked credits

• Verify expense eligibility

RCM Compliance

- Identify RCM transactions

• Pay GST under RCM

• Report properly in returns

Record Maintenance

- Maintain agreements

• Preserve invoices

• Keep payment records

• Maintain reconciliation statements

Annual Review

- Verify turnover thresholds

• Review e-invoicing applicability

• Conduct GST health check

• Review notices and litigation exposure

GST on Export of Professional Services

Export of services may qualify as zero-rated supply subject to conditions.

To qualify as export of services:

- Supplier should be located in India

• Recipient should be outside India

• Place of supply should be outside India

• Payment should be received in convertible foreign exchange or permitted modes

• Supplier and recipient should not merely be establishments of the same entity

Exporters may:

• Export under LUT without payment of IGST

OR

• Pay IGST and claim refund

Proper documentation is essential for export benefits.

GST for Freelancers and Independent Consultants

Freelancers are also covered under GST provisions if turnover crosses registration thresholds.

Common freelancers covered include:

- Content writers

• Designers

• Digital marketers

• Technology consultants

• Trainers

• Business consultants

• YouTubers and influencers in certain cases

Freelancers working with overseas clients should carefully evaluate export rules and foreign remittance documentation.

Common GST Mistakes Made by Professionals

Some common compliance mistakes include:

- Delayed GST registration

• Wrong place of supply determination

• Incorrect GST rate usage

• Failure to reconcile GSTR-2B

• Missing RCM liability

• Improper ITC claims

• Failure to maintain agreements

• Incorrect export treatment

• Non-compliance with e-invoicing

Regular compliance reviews help avoid notices and penalties.

Understanding the difference between tax planning and tax compliance helps professionals build a proactive approach to GST and income tax obligations — reducing litigation risk and improving financial efficiency year-round.

Penalties Under GST for Professionals

GST law prescribes penalties for various defaults.

Possible consequences may include:

- Late fees for delayed returns

• Interest on delayed tax payment

• Penalty for non-registration

• Wrong ITC claims

• Incorrect invoicing

• Non-payment under RCM

• Non-compliance with e-invoicing

Maintaining proper records and periodic compliance reviews reduces litigation risk.

Technology and GST Compliance

Technology has become important for GST management.

Professional firms now commonly use:

- GST-enabled accounting software

• Automated reconciliation tools

• E-invoicing integration systems

• Cloud accounting platforms

• GST analytics dashboards

Automation helps reduce manual errors and improve reporting accuracy.

Conclusion

GST compliance for professional services has become more structured and technology-driven. Professionals and consulting firms must carefully monitor registration thresholds, invoicing requirements, reverse charge provisions, ITC eligibility, and filing obligations.

With the introduction of e-invoicing for higher turnover firms and the structural changes introduced under the Income Tax Act, 2025 relating to TDS reporting, businesses should strengthen compliance systems and documentation practices.

A proactive approach helps reduce litigation risk, avoid penalties, improve client confidence, and maintain smooth business operations.

Professional firms should periodically review GST applicability, conduct reconciliations, and obtain professional guidance wherever required.

References

- Central Goods and Services Tax Act, 2017

- GST Notifications and Circulars relating to professional services and reverse charge mechanism

- Income Tax Act, 2025 — Section 393 references

- Income Tax Department FAQs and section mapping documents

Frequently Asked Questions

- Is GST mandatory for professionals in India?

GST registration becomes mandatory if aggregate turnover exceeds ₹20 lakh for most states or ₹10 lakh for special category states, subject to applicable conditions.

- What is the GST rate for professional services?

Most professional services are taxable at 18% GST unless specifically exempted.

- Is e-invoicing mandatory for professional firms?

Professional services firms crossing prescribed turnover thresholds, including ₹5 crore turnover applicability as per current requirements, are required to comply with e-invoicing provisions.

- Can professionals claim input tax credit?

Yes. Professionals may claim ITC on eligible business expenses used for providing taxable services, subject to GST conditions.

- Does reverse charge apply to legal services?

Yes. Certain legal services provided by advocates to business entities are generally covered under reverse charge mechanism.

- What is the GST registration limit for service providers?

The standard threshold is ₹20 lakh, while special category states generally have a ₹10 lakh threshold.

- What changed under TDS Section 393 from April 2026?

The Income Tax Act, 2025 reorganised TDS provisions into a new structure, including Section 393 for specified non-salary payments relating to professional and related services.

Introduction

Goods and Services Tax (GST) has changed the taxation system for service providers in India. Professionals such as Chartered Accountants, lawyers, consultants, architects, engineers, doctors, freelancers, management advisors, designers, and technology consultants are now required to understand GST compliance carefully.

Many professionals still have practical doubts about GST registration, invoicing, reverse charge mechanism (RCM), input tax credit (ITC), e-invoicing, TDS provisions, and filing requirements. Incorrect GST compliance may lead to notices, penalties, delayed refunds, and tax disputes.

This updated guide explains GST for professional services in simple language for business owners, consultants, freelancers, and professional firms. The article also includes the latest 2026 updates relating to e-invoicing, reverse charge mechanism, and the new TDS Section 393 framework under the Income Tax Act, 2025.

This article is prepared for the website of PKC India, a professional services firm providing taxation, audit, advisory, and compliance services to businesses across India.

What is GST for Professional Services?

GST for professional services refers to the tax applicable on services provided by professionals and consultants. Under GST law, services provided for consideration during the course or furtherance of business are generally taxable unless specifically exempted.

Professional services may include:

- Chartered Accountancy services

• Legal services

• Consultancy services

• Technical advisory

• Engineering services

• Architectural services

• Interior design services

• Digital marketing consultancy

• Financial advisory

• IT consultancy

• Business management services

• Freelancing services

Most professional services attract GST at 18%, unless specifically exempted under law.

Who is Considered a Professional Under GST?

The GST law does not provide a single comprehensive definition for “professional services.” In practice, professional services generally refer to specialised services provided based on qualification, expertise, training, or technical knowledge.

Professionals may operate as:

- Proprietorship firms

• Partnership firms

• LLPs

• Private limited companies

• Independent freelancers

GST applicability depends on the nature of services and turnover thresholds.

GST Registration Threshold for Professional Services

One of the most important questions asked by consultants and professionals is whether GST registration is mandatory.

Under GST law, service providers are generally required to obtain GST registration if aggregate turnover exceeds:

- ₹20 lakh in a financial year for normal category states

• ₹10 lakh in a financial year for special category states

Special category states generally include certain North-Eastern and hill states as notified under GST law.

Aggregate turnover includes:

- Taxable services

• Exempt services

• Export services

• Interstate supplies

The threshold applies on an all-India basis under the same PAN.

When GST Registration Becomes Mandatory Even Below Threshold

Certain situations may require GST registration even if turnover is below ₹20 lakh.

Examples include:

- Interstate taxable supplies in specified situations

• E-commerce operator-related services in certain cases

• Reverse charge applicability

• Voluntary registration

• Input tax credit planning

• Requirement by clients or contracts

Professionals should evaluate registration applicability carefully before assuming exemption.

GST Rate for Professional Services

Most professional services are taxable at 18% GST.

This usually consists of:

- 9% CGST + 9% SGST for intra-state services

OR

• 18% IGST for interstate services

Examples of services generally taxable at 18%:

- CA services

• Legal consultancy by law firms

• Management consultancy

• Engineering consultancy

• IT consultancy

• Recruitment consultancy

• Interior design services

• Marketing consultancy

However, some services may be exempt under specific notifications.

GST Exemptions for Certain Professional Services

Certain professional services may enjoy GST exemption subject to conditions.

Examples may include:

- Healthcare services by clinical establishments and authorized medical practitioners

• Certain educational services

• Services provided by advocates to non-business entities in specified cases

• Agricultural extension services in specified cases

Exemptions depend on the exact nature of services and recipient category. Professionals should verify exemption notifications carefully before treating services as exempt.

Time of Supply for Professional Services

Under GST, tax liability generally arises at the earlier of:

- Date of invoice

OR

• Date of payment

Professionals should issue invoices within prescribed timelines to avoid compliance issues.

For continuous or long-term consultancy assignments, contract terms and milestone-based billing should be properly documented.

Place of Supply for Professional Services

Determining the place of supply is important because it affects whether CGST-SGST or IGST is charged.

For most B2B professional services:

Place of supply is generally the location of the registered recipient.

For B2C services:

Place of supply may depend on the location of the recipient or supplier based on the nature of services.

Incorrect place of supply determination may result in wrong tax payment and future disputes.

GST Invoice Requirements for Professional Services

A GST invoice for professional services generally contains:

- Name and address of supplier

• GSTIN

• Invoice number and date

• Client details

• Description of services

• SAC code

• Taxable value

• GST rate and tax amount

• Place of supply

• Signature or digital authentication

Professionals should maintain proper invoice numbering and documentation systems.

SAC Code for Professional Services

SAC stands for Services Accounting Code.

Different professional services fall under different SAC classifications.

Examples:

- Accounting and auditing services

• Legal services

• Architectural services

• Information technology consultancy services

• Management consultancy services

Using the correct SAC code helps proper GST reporting.

Input Tax Credit (ITC) for Professional Services

Input Tax Credit is one of the most important benefits under GST.

Professionals can generally claim ITC on GST paid for business-related expenses used in the course of providing taxable services.

Examples where ITC may generally be available:

- Office rent

• Professional software subscriptions

• Internet expenses

• Office equipment

• Audit and consultancy expenses

• Business travel expenses

• Staff training expenses

• Telephone and communication expenses

However, ITC is subject to conditions and restrictions under GST law.

ITC Eligibility Table for Professional Services

Eligible for ITC

- Office rent used for business

• Laptop and computer purchases

• Accounting software

• Professional subscriptions

• Internet and telephone bills

• Office stationery

• Consultancy services received

• GST paid on business travel subject to conditions

Generally Restricted or Blocked ITC

- Personal expenses

• Motor vehicles in many cases

• Club memberships

• Food and beverages in many cases

• Personal travel expenses

• Employee-related personal consumption

• Expenses without proper GST invoices

Professionals should maintain proper documentation and vendor GST compliance checks before claiming ITC.

Composition Scheme for Professionals

Earlier, professionals had limited applicability under composition schemes. Over time, GST law introduced composition options for certain service providers subject to turnover conditions.

Professionals considering composition schemes should evaluate:

- Reduced compliance benefits

• Restrictions on ITC

• Restrictions on interstate supplies in certain cases

• Lower tax rates

• Client expectations regarding GST invoices

The decision should be based on business model and customer profile.

GST Returns Applicable to Professionals

Professionals registered under GST may be required to file:

- GSTR-1

• GSTR-3B

• Annual return in applicable cases

The return frequency may depend on turnover and the selected filing scheme.

Timely filing is important because delayed returns may result in:

- Late fees

• Interest liability

• ITC blockage

• Compliance notices

E-Invoicing for Professional Services Firms — Mandatory from ₹5Cr Turnover

E-invoicing has become an important compliance requirement under GST.

As applicable in 2026, businesses crossing prescribed turnover thresholds are required to generate e-invoices through the Invoice Registration Portal (IRP).

Professional services firms with aggregate turnover exceeding ₹5 crore are required to comply with e-invoicing requirements, subject to applicable GST notifications and amendments.

Under e-invoicing:

- Invoice data is uploaded to the IRP

• Invoice Reference Number (IRN) is generated

• QR code is generated

• Invoice becomes GST-compliant for reporting purposes

Applicability is determined based on aggregate turnover in preceding financial years.

Why E-Invoicing is Important for Professionals

E-invoicing helps:

- Reduce invoice mismatches

• Improve GST reporting accuracy

• Reduce fake invoice risks

• Simplify reconciliation

• Improve compliance tracking

Professional firms should ensure their accounting software is compatible with IRP integration requirements.

Consequences of Non-Compliance with E-Invoicing

If e-invoicing is applicable but invoices are not generated through the prescribed system:

- Invoice may be treated as invalid

• ITC issues may arise for clients

• GST penalties may apply

• Compliance notices may be issued

Therefore, firms crossing turnover thresholds should review applicability carefully.

What is RCM Under GST for Professional Services — Updated 2026 List

Reverse Charge Mechanism (RCM) means GST liability shifts from the supplier to the recipient in specified cases.

Certain professional services continue to fall under RCM in 2026.

Examples generally covered under RCM include:

- Legal Services by Advocates

Services provided by an advocate or firm of advocates to a business entity are generally covered under reverse charge subject to applicable conditions.

- Director Services

Services provided by directors to companies are generally covered under reverse charge under GST.

- Certain Services by Chartered Accountants and Professionals

Most CA services are generally taxed under forward charge. However, businesses should evaluate specific transactions carefully for RCM applicability wherever notified.

- Sponsorship Services

Certain sponsorship-related transactions may fall under RCM.

- Import of Services

Import of professional services may require GST payment under reverse charge.

Businesses receiving services under RCM must:

- Pay GST directly

• Report liability properly

• Maintain documentation

• Claim ITC subject to eligibility

Professionals should regularly review updated RCM notifications because applicability may change through amendments and clarifications.

New TDS Section 393 — What Changed from April 2026

From 1 April 2026, the Income Tax Act, 2025 introduced structural changes in TDS provisions.

The earlier TDS framework under Section 194J of the Income-tax Act, 1961 has now been reorganized under Section 393 of the Income Tax Act, 2025 for specified non-salary payments. citeturn0search0turn0search3turn0search12

The objective of the new structure is simplification and consolidation of TDS provisions.

Key practical points for professional services:

- Professional fees continue to attract TDS provisions

• Reporting structure has changed under the new Act

• Section references in returns and certificates may change

• Businesses should update accounting and ERP systems accordingly

As per available guidance and mapping documents, the old Section 194J references relating to professional fees have been mapped into Section 393 structures under the Income Tax Act, 2025. citeturn0search1turn0search3turn0search12turn0search13

Businesses and professionals should consult tax advisors for updated compliance procedures under the new framework.

GST Compliance Checklist for CA Firms and Consultants

Professional firms should maintain a practical GST compliance process.

Basic GST Checklist

Registration

- Verify GST registration applicability

• Update principal place of business

• Review additional place registrations

Invoicing

- Use correct GST rates

• Mention SAC codes

• Verify client GSTIN

• Generate e-invoice where applicable

Returns

- File GSTR-1 on time

• File GSTR-3B on time

• Reconcile turnover periodically

ITC Review

- Match vendor invoices

• Reconcile GSTR-2B

• Review blocked credits

• Verify expense eligibility

RCM Compliance

- Identify RCM transactions

• Pay GST under RCM

• Report properly in returns

Record Maintenance

- Maintain agreements

• Preserve invoices

• Keep payment records

• Maintain reconciliation statements

Annual Review

- Verify turnover thresholds

• Review e-invoicing applicability

• Conduct GST health check

• Review notices and litigation exposure

GST on Export of Professional Services

Export of services may qualify as zero-rated supply subject to conditions.

To qualify as export of services:

- Supplier should be located in India

• Recipient should be outside India

• Place of supply should be outside India

• Payment should be received in convertible foreign exchange or permitted modes

• Supplier and recipient should not merely be establishments of the same entity

Exporters may:

• Export under LUT without payment of IGST

OR

• Pay IGST and claim refund

Proper documentation is essential for export benefits.

GST for Freelancers and Independent Consultants

Freelancers are also covered under GST provisions if turnover crosses registration thresholds.

Common freelancers covered include:

- Content writers

• Designers

• Digital marketers

• Technology consultants

• Trainers

• Business consultants

• YouTubers and influencers in certain cases

Freelancers working with overseas clients should carefully evaluate export rules and foreign remittance documentation.

Common GST Mistakes Made by Professionals

Some common compliance mistakes include:

- Delayed GST registration

• Wrong place of supply determination

• Incorrect GST rate usage

• Failure to reconcile GSTR-2B

• Missing RCM liability

• Improper ITC claims

• Failure to maintain agreements

• Incorrect export treatment

• Non-compliance with e-invoicing

Regular compliance reviews help avoid notices and penalties.

Penalties Under GST for Professionals

GST law prescribes penalties for various defaults.

Possible consequences may include:

- Late fees for delayed returns

• Interest on delayed tax payment

• Penalty for non-registration

• Wrong ITC claims

• Incorrect invoicing

• Non-payment under RCM

• Non-compliance with e-invoicing

Maintaining proper records and periodic compliance reviews reduces litigation risk.

Technology and GST Compliance

Technology has become important for GST management.

Professional firms now commonly use:

- GST-enabled accounting software

• Automated reconciliation tools

• E-invoicing integration systems

• Cloud accounting platforms

• GST analytics dashboards

Automation helps reduce manual errors and improve reporting accuracy.

Conclusion

GST compliance for professional services has become more structured and technology-driven. Professionals and consulting firms must carefully monitor registration thresholds, invoicing requirements, reverse charge provisions, ITC eligibility, and filing obligations.

With the introduction of e-invoicing for higher turnover firms and the structural changes introduced under the Income Tax Act, 2025 relating to TDS reporting, businesses should strengthen compliance systems and documentation practices.

A proactive approach helps reduce litigation risk, avoid penalties, improve client confidence, and maintain smooth business operations.

Professional firms should periodically review GST applicability, conduct reconciliations, and obtain professional guidance wherever required.

References

- Central Goods and Services Tax Act, 2017

- GST Notifications and Circulars relating to professional services and reverse charge mechanism

- Income Tax Act, 2025 — Section 393 references

- Income Tax Department FAQs and section mapping documents

Frequently Asked Questions

- Is GST mandatory for professionals in India?

GST registration becomes mandatory if aggregate turnover exceeds ₹20 lakh for most states or ₹10 lakh for special category states, subject to applicable conditions.

- What is the GST rate for professional services?

Most professional services are taxable at 18% GST unless specifically exempted.

- Is e-invoicing mandatory for professional firms?

Professional services firms crossing prescribed turnover thresholds, including ₹5 crore turnover applicability as per current requirements, are required to comply with e-invoicing provisions.

- Can professionals claim input tax credit?

Yes. Professionals may claim ITC on eligible business expenses used for providing taxable services, subject to GST conditions.

- Does reverse charge apply to legal services?

Yes. Certain legal services provided by advocates to business entities are generally covered under reverse charge mechanism.

- What is the GST registration limit for service providers?

The standard threshold is ₹20 lakh, while special category states generally have a ₹10 lakh threshold.

- What changed under TDS Section 393 from April 2026?

The Income Tax Act, 2025 reorganised TDS provisions into a new structure, including Section 393 for specified non-salary payments relating to professional and related services.